Apr 7, 2021 AT 10:21PM

US stocks closed mixed with S&P 500 hit a record high in thin volume while small caps were the days biggest losers tumbling by 1.5% with Nasdaq holding modest gains and the Dow/S&P closed flat. Nasdaq continued its significant outperformance over Small Caps, surging to its strongest since mid-Feb (reversing around The March FOMC meeting). FOMC minutes once again were interpreted as dovish as Fed continued commitment to accommodative policy to support a full economic recovery as it refrained from signalling it will make any changes to its QE program any time soon. Fed Funds futures were active after Chair Powell acknowledges it might be appropriate to implement adjustments to administered rates at upcoming meetings or even within meetings if undue downward pressure on overnight rates emerged (Hikes on IOER and ON RRP remain in play I guess). Elsewhere, Yields were choppy with 10YR closed around 1.66%. Junk bond spreads compressed to their tightest since 2007, back below 300bps. Cryptos puked with Bitcoin back <$56k and Ether <$2k. Crude tumbled on last nights API, tested $60 overnight, then tumbled again on the official EIA data only to bounce off $58 to end higher on the day.

Mar 29, 2021 AT 09:44PM

US stocks closed mixed with Dow rose to a new record helped by Boeing (+2.3%) after Southwest Airlines added 100 orders for the airliners 737 Max jet, although Financial and energy shares pushed the SPX down from a record high following Archegos liquidation. The sell off extended just after the US cash open led by small caps which closed lower by 2.5% although stocks did manage to bounce at the EU close after MS said it had no more blocks to sell but the bounce did not last as headlines hit into the last hour of Wells Fargo selling blocks which saw shares of Viacom, GSX, Vipshop, farfeth and iQIYI all closed near session lows. Elsewhere, Banks stocks tumbled with MS, WFC worst on the day. Bonds were also battered with US 10YR tops above 1.70%. Credit markets also felt the small ripples of the forced unwind. Oil remained in its recent range and rebounded of its $60 support lvl. Precious metals were dumped with Gold nears $1700 and Silver fell below $25 handle while Cryptos were bid with Bitcoin surges to $58k while Ethereum tops $1800.

Mar 28, 2021 AT 07:04PM

1) Covid-19 and Vaccine rollout

2) Suez Canal Blockage

3) BOJ Summary of Opinions (Mon)

4) Joe Biden’s $3Trl infrastructure package (Wed)

5) China PMIs (Wed)

6) EU HICP Data (Wed)

7) Opec+ meeting (Thurs)

8) US ISM Manf (Thurs)

9) NFP (Fri)

10) M/Qty End Rebal

Mar 24, 2021 AT 11:12PM

US stocks closed sharply lower after tech sell-off resumed with Nasdaq closed lower by 2%. Energy, Banks were the best performers while tech lagged. Momentum was crashed over Value with the ratio plunging by almost 12%. Oil jumped with Crude futures rising more than 5% after the Suez Canal blockage sparked a panic bid in crude despite significant crude builds. This was WTIs best day since early Nov (the vaccine headlines). The dollar was also bid and is back to 2-week highs with BBDXY at $1150 handle and DXY testing its 200dMA. Cryptos were sold off with Bitcoin erased entire Elon Musk tweet gains and plunges back to $52k lvl while Ether dropped <$1600. Bonds were roller-coaster (bid during Asia, dumped during Europe, bid during US), but ended lower in yield on the day with US 10yr yields dropped back at 1.60%. This is the 3rd daily yield drop in a row, the longest streak since Dec 14th.

Mar 23, 2021 AT 09:15PM

US stocks closed sharply lower as the sell-off extended in late afternoon led by small-cap stocks with Russell index tumbling by 3.6% as virus cases and new restrictions in Germany signal the global reopening will be delayed. Travel and retail stocks sold off heavily with Carnival and Norwegian cruise lines slumped >7% each. American Airlines and United Airlines also dropped more than 6%. Energy stocks were also sold off as Crude crashed on demand fears (European lockdowns) and supply anxiety (floating storage unwinds) which slammed WTI below $58 to six-week lows (and below its 50DMA). Also, Oil time spreads are now flipped into contango. Elsewhere, the dollar strengthened across g8 peers with Antipodeans the worst performer – kiwi$ fell almost 2% while the 10-year US Treasury yield slid for a second day after Powell played down the risk that economic growth would spur unwanted inflation. Meanwhile, Powell also stressed that when it’s time to taper, the CB will communicate carefully and move slowly. Cryptos were unchanged today holding losses for the week while Commodities were all sold off as the dollar rallied but copper and crude got hit worst and Silver fell to $25 handle.

.PNG)

Mar 22, 2021 AT 08:39PM

US stocks closed higher led by tech shares as treasury yields retreated from the highest levels and slid back below 1.70%. The tech-heavy Nasdaq gained 1.2% to 13,377 and the S&P 500 rose 0.7% to 3,940 breaking a two-day losing streak while the Dow climbed 100 points to 32,731. Apple, Microsoft, and Netflix all gained at least 2%, while Amazon and Facebook climbed more than 1% each and Tesla closed higher by 3.5% post Cathie Wood’s Ark massive price f/cast. Big tech was aggressively bid from the second the cash market opened while the small caps were slammed with Nasdaq had its best day vs Small Caps since the vaccine headlines in early November. Sector wise - Banks, Airlines all plummeted vs Tech outperformed. Elsewhere, Turkey was the focus today with Lira plunging by almost 10% after Erdogan fired yet another central bank head over the w/e . The dollar retraced its losses from the FOMC last week, then dumped and close <$1140. The US 10YR yields fell back <1.70% again with the bond market remains in focus this week amid a slew of Treasury auction and Fed speakers along with Fed chair Jerome Powell and Treasury Secretary Janet Yellen are expected to make their first joint appearance on Tuesday.

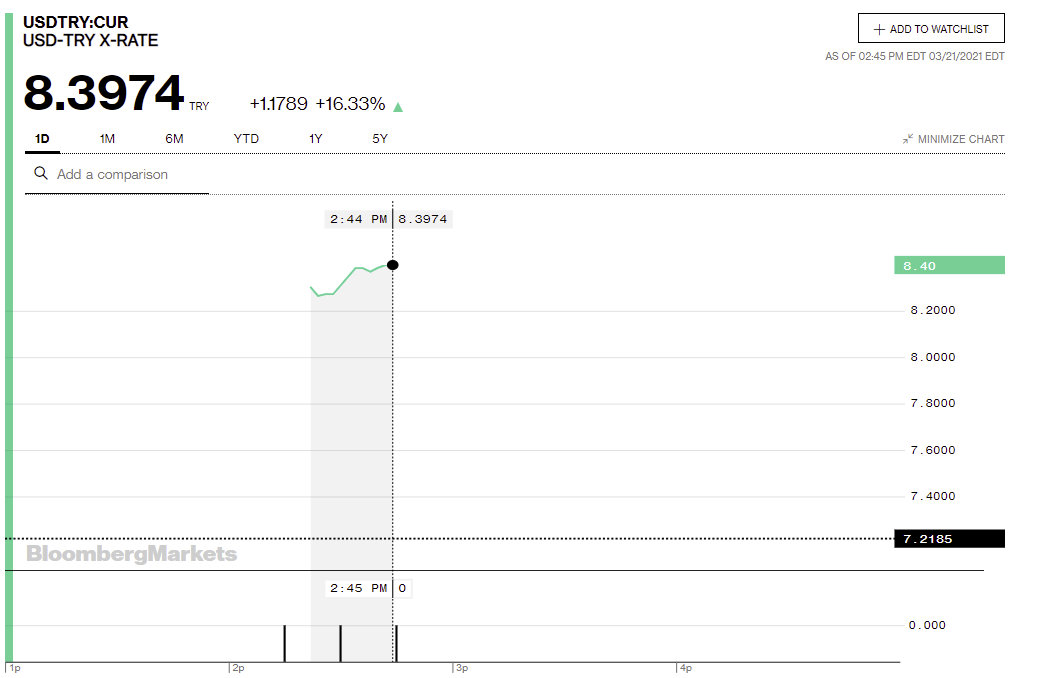

Mar 22, 2021 AT 09:08AM

Post CB governor removal over the weekend just 2 days after 200bps rate hike. Infact, This is the 4th time a TCMB Governor has been replaced in the last two years, following the removal of Murat Cetinkaya from his post in July 2019 and the removal of Murat Uysal from his post in November 2020. Here are the key Assets performance this morning.

1) BIST Index -10%

2) Lira Collapsed - $TRY rallied as much at 17% to >8.45 on Sunday night open before settling at 8 handle.

3) Turkey 10YR Bond yield up by 17%

4) Turkey 5Y CDS 425/460 +130

5) IQQ5 GY (iShares MSCI Turkey) plunges 20%

Mar 18, 2021 AT 08:47PM

US stocks fell from record highs as spike in Treasury yields dented demand for tech shares with high valuations, sending the Nasdaq 100 Index tumbling 3.1% as Apple, Amazon and Netflix all fell more than 3% and Tesla slipped nearly 7%. The rout in risk assets picked up in the afternoon, starting with a selloff in crude. Oil plunged 8% on concern new restrictions in Europe will hamper demand. On the day, Nasdaq and Small Caps were both smashed and the Dow outperformed but was still lower. Today was Nasdaqs 2nd biggest down day since October. The 10-year Treasury yield jumped 11bps to >1.75% at its session high, reaching its highest level since Jan20. The 30-year rate also climbed 6bps at one point, breaching the 2.5% level for the first time since Aug 2019. Sector wise, Banks dramatically outperformed big-tech and are now back at their strongest (relatively) since early March 2020 with JPM +1.7%, BofA gained +2.6%. The energy sector was the biggest loser with a 4.7% decline, ARKK was also hammered along with Tesla with etf closed -6%. The dollar jumped at the European open and US open, erasing much of yesterdays Powell pummelling with BBDXY close at $1140 and Bitcoin briefly topped $60k before drifting back to $57.5k.

Mar 17, 2021 AT 08:55PM

US stocks erased earlier losses to close higher on the day with S&P climbing to the highest level on record while Dow tops $33k and close at an all-time high after the Fed said it sees near-zero interest rates at least through 2023 despite rising inflation concerns. The Nasdaq also wiped-out earlier losses of almost 1.5% and ended the day 0.4% higher. Despite the dovish statement, 5yr yields outperformed and the 5s30s yield curve steepened dramatically to a level not seen since 2014. Meanwhile, Fed Chair Jerome Powell said in a press conference that the Fed would need to see a material and sustained move in inflation above 2% before considering changes to its current easy policy stance. Elsewhere, US 10yr yields retreated from its highs of the day from 1.69% to 1.62%. The dollar tumbled versus most major peers with Bloomberg dollar index fell from $1142 to $1135 handle. Commodities all rallied as the dollar retreated with Bitcoin and Silver exploded while Crude ended the day lower.

Mar 16, 2021 AT 08:42PM

US stocks flipped between gains and losses as the Dow fell from its record high and snapped seven-day winning streak ahead of crucial FOMC meeting tomorrow. The market fell to its session lows when the benchmark 10-year Treasury yield briefly rose above 1.62% in the afternoon trading with Energy, Airlines and Industrials led the declines. Apple and Microsoft lifted the tech-heavy Nasdaq 100, while the Dow fell from a record high, with Boeing and Goldman Sachs among the biggest decliners. Nasdaq was panic bid at the US cash open while small caps smoked, this was Nasdaq biggest outperformance over Small Caps since November 4th and the move erased the entire last week’s relative small cap index outperformance. Elsewhere, Bond’s struggle to find direction with US 10YR traded range bound from 1.58% to 1.62% all day before rallying near to the close to 1.62%. Oil retreated for a third day, while the dollar was mixed versus its major peers and Bitcoin traded around $56k.

Mar 16, 2021 AT 10:54AM

Mar 15, 2021 AT 09:43PM

US stocks reversed dramatically higher at the EU close with both the Dow and S&P hit new record highs. The DJIA rose by 175 points to a record close and finished up for a seventh session in a row, the longest winning streak since August. The benchmark S&P 500 Index gained for a fifth straight trading session, led by Airlines, utilities, and real estate sectors. Apple, Tesla and Facebook led the mega tech-heavy Nasdaq higher. Jets etf close +4% with AAL and UAL shares rose 7.7% and 8.3%, respectively. Cruise liners also surged with Carnival and Royal Caribbean closed +5%. Elsewhere, Crude oil pared a loss of more than 2%, 10yr yields fell off the highs and held the 1.60% handle while 5Y Breakevens hit 2.60%, highest since 2008. Bitcoin pulled back after a weekend rally that sent prices above $61,000 for the first time and VIX briefly fell <20. All eyes on US retails sales tomorrow followed by the Fed on Wednesday.

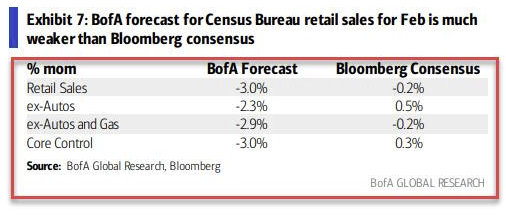

Mar 15, 2021 AT 07:15PM

As per latest aggregated monthly credit and debit card data, BAC finds a 2.3% M/M decline in core retail sales (ex-autos) in February, a drop which reflects three main factors:

As such, the banks measure of “core control retail sales”, which nets out autos, gas, building materials and restaurants is down 3.0% mom SA.

Mar 14, 2021 AT 05:54PM

Financial markets focus will shift to the US and UK over the coming week, as rate-setters in both jurisdictions meet to decide on policy, on Wednesday and Thursday, respectively. After a stunning selloff in US Treasuries which took benchmark 10-year yields above 1.6%, the highest in a year, the March 16-17 Federal Reserve meeting will be watched closely for hints policymakers are concerned about yields, asset bubbles and inflation and whether the Fed will decide to act on FI turbulence and prolong the Supplementary Leverage Ratio (SLR) relief beyond 31 Mar despite more and more Democrats voicing their concerns about doing so. As Nordea flagged, a non-prolongation scenario could lead to pent-up sales of as much as USD 700bn worth of US Treasuries. Other than fed, it’s a busy calendar of central bank meetings with BoE, BoJ and Norges Bank are all due next week. Last week, the BOC left monetary policy unchanged, however the ECB is feeling the pressure of rising yields and inflation expectations and said they will increase the pace of bond purchases significantly. Neither the Fed nor the BOE are expected to announce any policy changes but remarks from policymakers will be carefully parsed for any guidance regarding how the recent rise in government bond yields might, or may not, be influencing their thinking. Elsewhere, The US also has some key data points this week, notably industrial production, and retail sales.

1) FOMC (Wednesday)

The Federal Reserve will be meeting for the first time since yields exploded higher and the Biden stimulus bill became law. It’s FOMC week and the world will be watching what the Fed’s response will be to the spiked volatility in bond markets that’s upset tech stocks and revived the US dollar. What to watch?, As per ING - We’ll get to see a new set of quarterly projections, where 2021 GDP will likely be revised higher from the 4.2% median in December. There will also be a lot of interest in the Fed Funds rate Dot Plots. Does the Fed 2023 Dot Plot median shift to a 25bp hike? Probably not, but the dollar would probably rally if it did. Treasuries, there is huge focus on whether the Fed extends its US Treasury exemption from the SLR – due to expire at the end of the month. Failing to extend it would be a big surprise, hit Treasuries and also hit equities on the view that US banks would have to raise more equity capital.

Per Nordea - An operation Twist could be one way of mitigating the potential downside pressure on longer bonds from re-installing the SLR regulation, but we still find such action unlikely against the backdrop of increasing inflation. Should the Fed decide to move towards a WAM of 10yrs in the SOMA portfolio again, it could work to temporarily dampen the steepening pressure in the USD curve, but it may not work as well as in 2011-2012 as the business cycle is gaining momentum, which usually leads to higher bond yields, not lower. Mind the gap between the Global PMI and 10yr bond yields? We target 2% in the 10yr Treasury already towards summer.

2) BOE (Thursday)

Thursday brings central bank meetings in Britain and Norway. The BoE is not seen unveiling additional policy easing despite concerns over the recent spike in borrowing costs. Instead, any action such as upping the BoE’s bond-buying firepower is likely to come later in the year - perhaps in May, when the next set of economic forecasts emerge. The BoE should keep its constructive outlook in place, with the fast pace of vaccination (and the pace is poised to double from the next week onwards) supporting the optimistic outlook for the economic recovery.

3) NORGES BANK (Thursday)

In Norway, there is a clear scope for a hawkish revision of the outlook not least due to higher oil prices. At the rate meeting next week, Nordea expect Norges Bank to signal a first rate hike in December this year, with the probability that it’ll come as soon as September. Moreover, you should expect a higher rate path throughout the forecast period, mostly driven by oil prices but also by the vaccine roll-out. (Nordea)

ING on Norges Bank

The possible hawkish bias of the Norges Bank (NB) meeting next Thursday is likely to be another tailwind for NOK. Rising CPI, higher oil prices and optimistic prospects for the vaccination suggest further upward revision to the interest rate path – both in terms of bringing the timing of the first rate hike forward and raise the interest path across the forecast horizon. The upgrade to the interest rate path is likely to push EUR/NOK lower, with the psychological EUR/NOK 10.00 level likely to be seriously tested next week.

4) BOJ (Friday)

The Bank of Japan will present the review of its policy tools on Mar 18-19, which may carry important spillovers to global markets. The BOJ has tried to persuade markets that the review only aims at increasing the bank’s flexibility to counter potential new shocks, but bond markets have tested the yield-curve-control regime recently, with the 10yr bond yield trading above 15 bps just a few weeks back. The BOJ’s setup has become terribly “pro-cyclical” since it buys more bonds, when growth and bond yields are rebounding in tandem, while it buys less bonds when growth disappoints. Could the target be changed to get rid of the procyclicality? A lot is at stake and the BOJ will likely insert clearer guidance in its statement on what it sees as an acceptable level of fluctuation in long-term interest rates, according to sources -- a sign it won’t tolerate rises that hurt the economy. Given a nascent economic recovery, the BOJ may even suggest scope for more negative short-term rates. In the midst of this, financial year-end flows back into yen are accelerating. A currency rally will add to the BOJ’s headaches.

5) EM CB meetings (Brazil and Turkey)

In EM, meanwhile, the only way for interest rates to go may be up. That’s the message we might hear from several central banks over coming days. Central banks in Brazil and Turkey -- meeting on Wednesday and Thursday respectively -- are most likely to raise rates. Markets will also find out on Thursday if Indonesia’s rate-cutting cycle has come to an end. Most have faced rising inflation pressures for some time but now they are also confronted by higher U.S. Treasury yields, which raise borrowing costs for everyone. For oil importers, Brent crude prices above $70 is an added problem -- all this while economies are still reeling from the coronavirus impact.

--------------------------------------------------------------------------------------------------------------------------------------------------------------

Source: Nordea, Reuters, FT, ING, DailyFX and FXStreet

This report has been prepared by consolidating the data from various sources mentioned below with respective links.

https://corporate.nordea.com/article/64074/week-ahead-on-why-long-bond-yields-increase-during-qe

https://www.reuters.com/article/idUSKBN2B41C2

https://www.ft.com/content/a5428953-7740-47d1-b683-d19ecd226658

https://think.ing.com/articles/g10-fx-week-ahead-12032021

Mar 12, 2021 AT 04:29PM

Mar 12, 2021 AT 01:26PM

Mar 12, 2021 AT 09:48AM

BAML FLOW SHOW

Inflation thematic is confirmed by Nasdaq topping vs S&P 500; note epic reversal in deflationary Nasdaq vs. inflationary Russell implies 2020 marked secular low point for inflation and rates (Michael Hartnett)

Mar 12, 2021 AT 07:47AM

US 10yr briefly tops 1.60%

Recall, these decent charts from Nordea/@AndreasSteno and @enlundm on 10th March.

FOMC on 17th - 1.75% soon?

Mar 11, 2021 AT 09:49PM

The S&P and the Dow climbed to a record high led by a renewed rally in tech shares while the signing of Covid relief bill gave stocks a further boost. ARKK gained another 6% along with FAANG index which close +4% as Tesla popped 4.7%, while Apple, Fb, Alphabet and Netflix all advanced at least 3%. Chip stocks also jumped sharply with Nvidia and AMD rose by 4% while Xilinx popped 6%. Elsewhere, the dollar fell for the third consecutive day, the biggest slump since the election/vaccines in early Nov. Bonds were hammered despite ECB headlines move, amid a massive issuance (30Y and Verizon) but the selloff stalled after the 30Y auction which tailed by around 50bps with strong direct bidding. A wave of buying swept thru in ED futures after the auction, focusing on the dec 22 contract as per Bloomberg. Reflation etfs like Solar, Clean energy also ripped higher with Tan +10%, ICLN +6%. In Commods, Copper climbed above $9,000 a ton in London and oil advanced with WTI >$66 and Brent close just shy of $70 handle. Cryptos were well bid with Ether resumes back >$1800, Bitcoin surged back up near $58k.

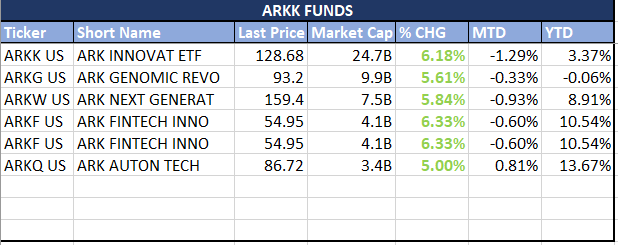

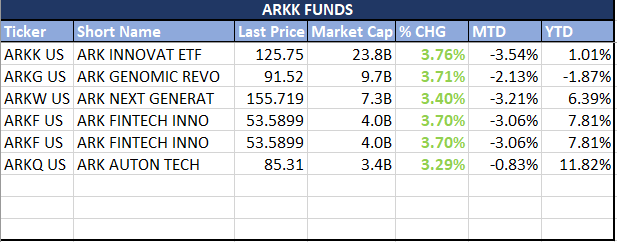

Mar 11, 2021 AT 03:27PM

ARKK funds having a good day, Flagship now up on the year..

Mar 11, 2021 AT 09:21AM

Short term technicals points towards a drop to 1.4%, lower bound of the short term uptrend channel.

ECB and 30yr bond auction next key event.

Mar 11, 2021 AT 08:47AM

Estoxx Vol extending further declines and is now below pre-pandemic lvls.

Mar 11, 2021 AT 07:11PM

Dow +1.5%, SPX +0.6%, Russell +1.9% and Nasdaq unch

RTY > NQA – ratio +2%

VaL > MoMo – ratio +2%

Dow >$32k, hit record highs

5YR Breakevens topped 2.5% - highest since July 2008

V2X < 20, VIX -6% to 22 handle

Bitcoin >$56k, Ether > $1800

US indices closed higher as the rotation into value extended following a weak CPI print with Dow and small caps outperformed mega-cap Nasdaq. The Dow soared more than 450 points and hit fresh record highs after treasury yields fell post 10yr note auction and house Democrats passing a $1.9trl covid relief bill. Energy (XLE +3.5%) and Financials (BKX +2.5%) were the best performers while tech lagged. Elsewhere, Bonds were aggressively bid during the US session as US 10yr fell towards 1.50%, 5YR Breakevens topped 2.5%, the highest since July 2008. The dollar weakened versus the G8 peers, Crude topped while real yields slipped and supported gold futures and Bitcoin briefly topped $57k.

Mar 10, 2021 AT 09:02PM

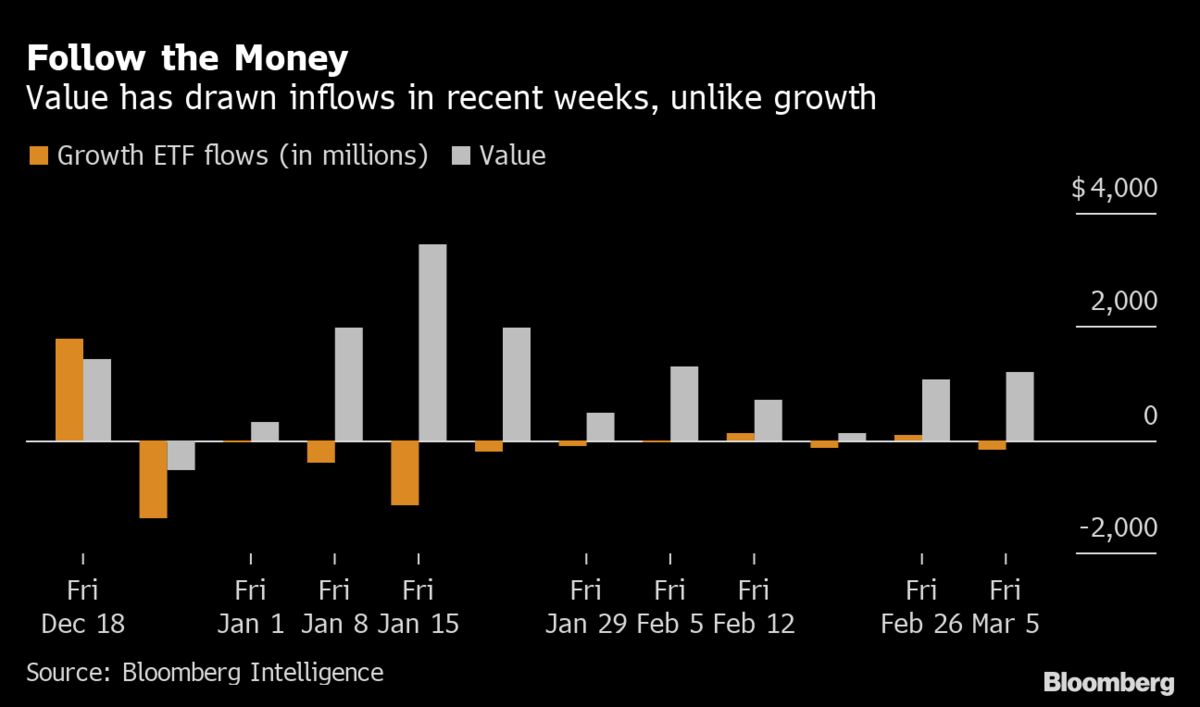

As part of the continued rotation out tech into Value, the value investing ETFs have brought in new money for 10 straight weeks. Assets have jumped $100 billion since the start of November. In fact, value investing, as a strategy, has now surpassed levels last seen before the pandemic, according to Bloomberg.

https://www.bloombergquint.com/markets/value-investing-gains-100-billion-and-wipes-out-pandemic-losses

Mar 10, 2021 AT 07:55PM

Despite the rout, Tech saw another near-record weekly inflow ($2.6B, the highest in over seven years). As a result, four-week average Tech flows have hit a new record high. (BofA)

Mar 11, 2021 AT 07:12PM

Nasdaq +3.7%, SPX +1.4%, Russell +1.9% and Dow +0.1%

MoMo > VaL – Ratio +18%

Solar (TAN) +13%, Clean Energy (ICLN) +8%

ARKK +10.5%, FAANG +7%, Tesla +20% and Apple, Amazon, and Facebook +4%

Gold > $1700 – closed +2%, Silver +3% to $26 and WTI tumbled by 2% to <$64 and Brent at $67

Bitcoin back >$1trl market cap as ccy nears $55k, Ether > $1800

US indices closed higher across the board led by tech heavy Nasdaq which climbed 3.7%, its best day since November. The index has now erased all of yesterday’s relative losses vs the Dow. The bounced in tech names was initially sparked in Asia after reports of China “National Team” stepped in and bought equities and then post US cash open - mega-cap techs, bonds, bullion all ripped higher. Momentum was heavily bid with the ratio over Value gained by almost 18%. Tesla exploded over 20% to its best day since Mar 2013, ARKK rose by 10%, its best day ever. Sector wise, Tech and Retail outperformed while Oil, banks, and Value sectors lagged. Elsewhere, Bond yields stabilized after US 10yr fell by more than 6bps to 1.53%. Dollar was weaker while cryptos were bid with Bitcoin back >$1trl market cap as ccy nears $55k and Ether >$1800. Oil was down for the second straight day with WTI fell by another 2% while Precious metals were bid with Gold bounced hard and >$1700 and Silver surged near $26.

Mar 9, 2021 AT 09:19AM

FTSE back above 6700 and above last week highs. Momentum picking up given reflationary shift and technicals looks solid.

Mar 9, 2021 AT 07:06AM

Nasdaq creating a decent H&S formation and is now below the Neckline. The difference b/w Head to Neckline points to a drop towards $11500 which is roughly where 200dMA sits. Tech rout is not over yet it seems.

Mar 11, 2021 AT 07:12PM

Nasdaq -2.5%, SPX -0.5%. Russell +0.8% and Dow +1%

MoMo < VaL – Ratio -6.5%

NQ < RT – Ratio -3.3%

ARKK -6%, FAANG -5% with Tesla -6%, Apple, Google, and Netflix -4%

Gold = $1680, Silver nears $25 and WTI reversed earlier gains to fell < $65.

US indices closed mixed as the rotation out of tech continues with Dow climbing by 300 points to record levels while the mega-cap tech index slid by 2.5%. As Bloomberg pointed out, it’s the first time since 1993, the Dow is at a record, while the tech-heavy Nasdaq is down around 10% from its high. Momentum meltdown extended with the ratio of value plunged by another 6% and is now down 35% over the last 5 sessions and -60% off Feb 9th peak. FAANG, ARKK also plummeted with Apple, Microsoft, Google closed lower by 4%. Elsewhere, Treasury yields were higher on the day but only modestly with US 10YR stable around 1.60%, the dollar strengthened and rallied to its highest close since early Nov. Crude reversed earlier gains to close lower on the day with Brent fell by 2% after soaring >$71. Cryptos extended gains with Bitcoin >$51k, Ethereum soared after the EIP-1559 approval while Gold, Silver fell with bullion dropped to $1680 lvl.

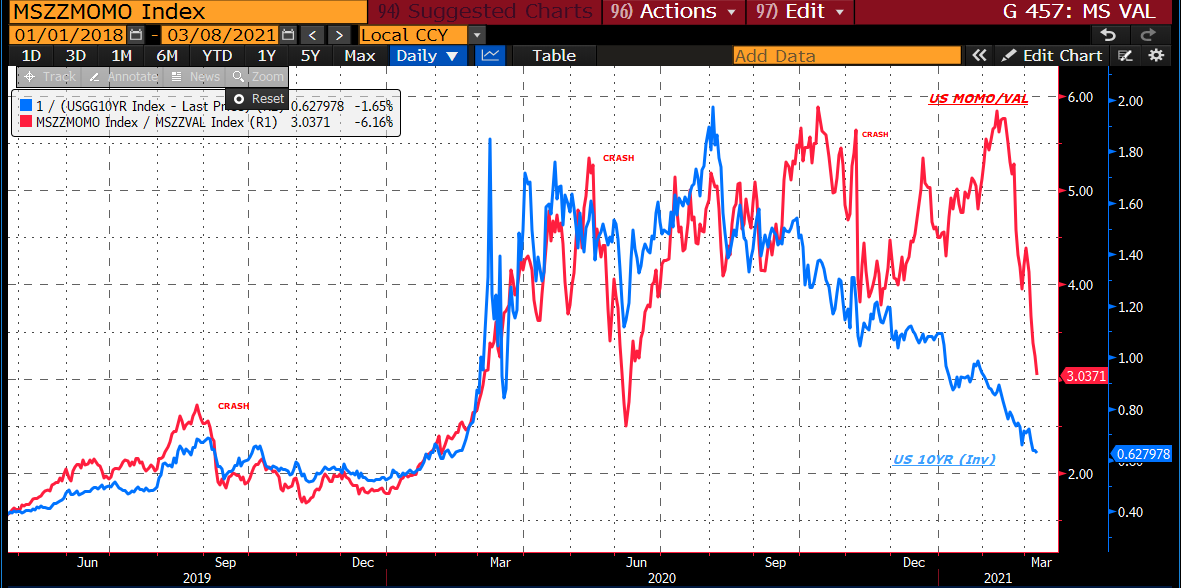

Mar 8, 2021 AT 07:14PM

Collapse in Momentum stocks continues, with the ratio over Value down another 6% and is -35% over the last 5 sessions and almost -60% since the Feb 9th peak.

Mar 8, 2021 AT 03:14PM

BIG lvl here for Estoxx futures, right at the highs of Feb last year and have tested multiple times this year. 4k next perhaps ?